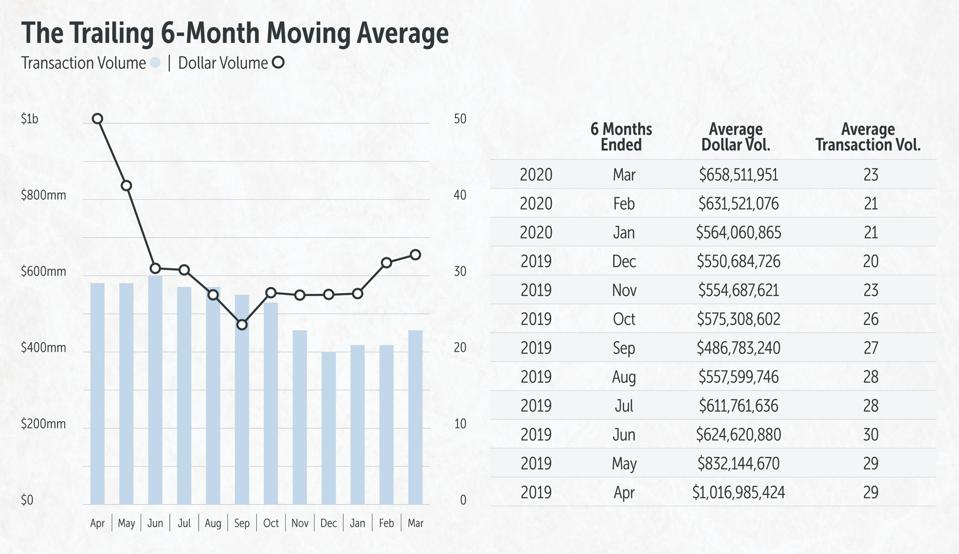

Trailing 6-Month Moving Average for Transaction Volume

Ariel Property Advisors

With the commercial real estate industry in a relative standstill right now, lenders have become increasingly cautious, particularly because rent collections are uncertain in the short term in every asset class. Instability in capital markets, rising unemployment and the free fall of public REITs have caused lenders to switch their approach from offense to defense.

For example, conventional balance-sheet lenders are especially careful. Covid-19 forced these lenders to extend forbearance to borrowers with unstable collections. Still, these lenders, while less active, are transacting with under-leveraged borrowers and closing transactions that were in the pipeline prior to the pandemic. Meanwhile, the current situation presents an opportunity to private lenders filling in the market gaps with shorter-term, relatively higher-rate loans.

Capital markets are active, but the landscape has shifted and you need to be strategic about your financing decisions. Here’s what you need to know.

Who’s Active?

It’s not really a surprise that private lenders are still active. Even before the crisis, they were typically open to deals that had underlying issues or higher risks. What’s changed is that bridge and mezzanine lenders, along with lenders offering two- or three-year terms, are now more open to longer-term and higher-capital deals, seeing opportunity where bank lenders may be holding off at the moment.

“This segment of lenders is going to offer high single-digit interest in a market where others are in a holding pattern,” says Matt Swerdlow, Director of Capital Services with Ariel. “This could help you keep your investment sales transactions moving forward under the right circumstances.”

“Debt funds are also still active,” he adds, “but keep in mind that these typically non-recourse, floating-rate loans usually only fund above the $10 million mark and are giving more scrutiny to deals.”

When a borrower defaults on a non-recourse loan, the lender can only cover its losses by retrieving the leveraged property, regardless of the current value of the property. Understandably then, hospitality and retail assets are particularly less attractive to these lenders, because the property values in these arenas are experiencing a great deal of long-term uncertainty.

Who’s Out?

Until last week, commercial mortgage-backed securities were a non-starter for most borrowers, unless the asset was in an ultra-prime location and had exceedingly low debt. Investors who already had CMBS deals in progress were seeing them dropped or the pricing changed dramatically.

However, the CMBS market reopened last week (May 4) with a new $771.9 million conduit offering from Goldman Sachs GSBD and Citigroup C . The move signals that lenders are starting to look for new business, quoting 10-year deals with loan-to-value ratios of up to 70%.

While there is still a great deal of uncertainty in CMBS markets, investors are starting to dip their toes back in the water and, with the right property, the numbers could make sense for financing, but this will very much be on a case by case basis.

What About Large Banks?

As I mentioned, traditional balance-sheet lenders are being highly conservative, focusing mainly on what they see as more bankable asset classes, such as multifamily and industrial. This isn’t to say that all balance-sheet lenders will be open to discussing your deal, even if you have a solid industrial property in a strong geographical market.

“There’s an abundance of caution right now,” says Eli Weisblum, Director of Capital Services with Ariel. “Some lenders aren’t looking at new deals until they reassess the market situation, while others are tightening their underwriting guidelines or will only consider repeat clients.”

Fannie Mae and Freddie Mac, for example, are experiencing a record number of loan applications and they are revising their loan policies to be more stringent as a result.

“It’s a lender’s market right now, and each one is going to approach this differently,” says Weisblum.

Even before the crisis, industrial was a strong market for investment sales, and capital sources were already confident in this class. Now, manufacturing is more essential than ever, with many firms pivoting to producing highly in-demand products, such as PPE or respirators, for the pandemic. If you have an industrial deal—and there aren’t any fundamental issues—you should be able to find balance-sheet lenders that are interested. Other properties such as some medical offices, government offices, self-storage facilities, data centers and Section 8 housing present great collection stability and are therefore in demand from conventional lenders.

Other asset classes present very different opportunities for lenders and debt funds. Retail and hospitality, in particular, will be difficult for capital transactions. Before the crisis, retail was already a struggling sector, especially in secondary urban markets. Even in prime markets like New York City, vacancy rates were high, and with the lockdown, that number is only going to increase. The sad reality is that many businesses are not going to survive this, even with the creative ways many are finding to stay open.

As a result, debt funds are already buying mortgage notes right now at steep discounts. This action allows a lender to sell the mortgage note and avoid a long and expensive foreclosure process. The lender can write the mortgage off as a loss today to free up capital tomorrow.

Strong Borrowers Will Benefit

There is still lender activity today and, as the situation stabilizes, there will be more lenders providing financing. As an investor, the type of property and location will determine the opportunities, but overall, the cost of capital will be low for the foreseeable future. This presents a tremendous financing opportunity for borrowers. While the lending market is going through an adjustment, well-positioned, under-leveraged assets and sponsors will benefit from current market conditions.