Boosting your credit score can save you big on interest costs.

Getty

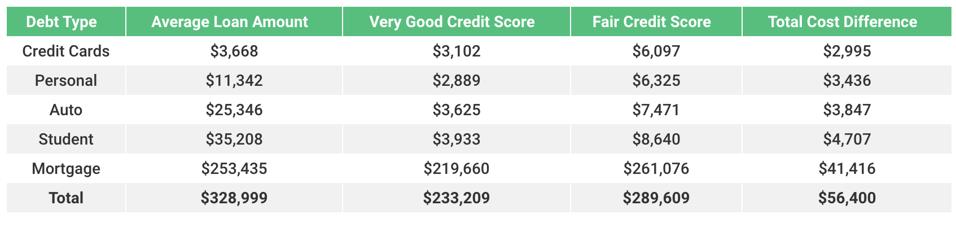

It pays to have good credit. In fact, bumping your score from the “fair” range to the “very good” range could save you a whopping $41,000 on your mortgage (and thousands on student, car and personal loans, too).

A new study from loan marketplace LendingTree shows the stark difference in interest costs across credit score tiers. Borrowers with “fair” scores—those between 580 and 669—pay significantly more than those in the “very good” range of 740 to 799. In fact, “fair” borrowers pay anywhere from $2,995 to upwards of $41,400 more over time.

The discrepancy is biggest on mortgages. The average mortgage borrower with a “very good” credit score pays just $219,660 in interest over time. “Fair” score borrowers pay a shocking $261,076.

There’s also a big difference in the amount of interest paid on student loans. While borrowers with “fair” scores pay an average of $8,640, those with “very good” scores pay only $3,933.

This chart shows the difference in interest paid across credit tiers.

Courtesy of LendingTree

In total, the analysis shows that borrowers with a fair score will end up paying over twice as much interest on personal, car and student loans, and 97% more on their credit cards.

For Americans holding the average debt across all five categories (credit cards, personal loans, car loans, student loans and mortgages), they could save more than $56,000, or around $316 per month, just by bumping their credit score from the “fair” to “very good” range.

If making that jump—which could mean increasing your score as much as 160 points—seems too difficult, LendingTree’s senior research analyst Kali McFadden says it’s important to see the bigger picture.

“The idea of managing your credit score can be intimidating and seem like a lot of effort,” she says. “The good news is that it’s not as complicated or opaque as many people fear, and it isn’t remotely comparable to the time, effort and stress it takes to work for a net $56,400.”

Want to increase your score and start saving on interest costs? Here are some expert hacks on how to do it—and do it quickly:

Don’t close those old cards out.

“The length of your credit history makes up about 15% of your credit score. If you have credit cards that you no longer use, try to keep them open as long as you’re not paying any annual fees to do so. Your old cards will help keep your credit utilization rate low, because it ups your overall limit, assuming you’re able to keep your spending in check.” — Bethy Hardeman, personal finance expert at Tally

Pay your bills mid-month.

“Your credit utilization ratio—the credit you’re using divided by your total credit limit—is usually reported as of your statement date, so it could be high even if you pay your bills in full and avoid interest. For example, if you have a $5,000 credit limit and you make $4,000 of charges throughout the month, that’s an 80% ratio, which is very high. A good solution is to make an extra mid-month payment and knock your balance down before the statement even generates.” — Ted Rossman, industry analyst at CreditCards.com

Ask for a credit limit increase.

“Ask for increases to your credit limit on existing accounts or open new lines of credit. By increasing the amount of credit you have available, your debt-to-credit ratio will lower. This will only work if you don’t add new debt.” — Natalie Graham, founder at GoFromBroke.com

Steer clear of late payments.

“Consistently paying your bills on time is the best thing you can do to raise your credit score, because payment history is the biggest factor influencing your score. A single late payment can drop an excellent credit score by 100 points or more, according to FICO data, and it stays on your credit report for seven years, so always paying on time is essential for raising your score and keeping it high. Set up automatic payments or reminders for yourself if you’re worried about forgetting.” — Nathan Hamilton, industry analyst and director at The Ascent

Check your credit report annually and report any errors immediately.

“Report errors on your credit reports. You can get them for free at AnnualCreditReport.com. The FTC says 20% of Americans have errors on their credit reports and 5% have major mistakes. Look for debts that don’t belong to you, late payments that you believe were on-time, etc.” — Rossman

Consider a personal loan if you have lots of credit card debt.

“If you have a lot of credit card debt, a personal loan can be beneficial to your credit score. Personal loans are a way to consolidate credit card debt on a fixed repayment plan, often lowering both your interest rate and your monthly payments. When you take out this type of loan to pay off credit cards in full, you have the potential to experience a significant bump in your credit score by eliminating the debt.” — Lauren Anastasio, certified financial planner at SoFi

Mix up your credit.

“Consumers with the best credit scores tend to use a mix of different types of accounts, including installment accounts (mortgages, auto loans and/or personal loans) and revolving accounts like credit cards. If you only have a credit card—or no credit cards—you may not score as well for this factor. Consider rounding out your credit history with a secured card or a credit-builder account to build strong credit.” — Gerri Detweiler, education director at Nav.com

Become an authorized user on someone else’s account.

“As an authorized user, you are added to someone else’s credit card account as a secondary account holder. You typically receive a credit card associated to this account and can use it to make purchases, but you are technically not responsible for payments on the account and you don’t have the ability to make changes to the account. The account payments and credit management is recorded on your credit report so you can benefit from the primary cardholder’s positive credit habits. But beware as this can also backfire. If the credit card owner misses a payment or rings up a hefty credit card bill, the negative behaviors can ding your score so just make sure you trust this person is financially savvy. Stick with a family member like a parent or spouse.” — Andrea Woroch, budgeting expert

Get a secured card.

“If card issuers won’t give you the time of day because you have a bad credit history, open a secured credit card instead. They require a security deposit that’s usually equal to your credit limit, but they’re open to everyone, regardless of their credit score. Used responsibly, they can help raise your score over time. If you decide to cancel the card in the future, your card issuer will refund your deposit, assuming you don’t have an outstanding balance.” — Hamilton