Millions of Americans unable to pay their rent during the pandemic face a snowballing financial burden that threatens to deplete their savings, ruin their credit and drive them from their homes.

A patchwork of government action is protecting many of the most financially strapped tenants for now. But it could take these renters — especially low-income ones — years to recover, even as the rest of the economy begins to rebound.

“Even if they say we can pay [missed rent] back in two or three years — that’s money we don’t have,” said Kelly Wise, a 32-year-old resident of L.A.’s Westlake neighborhood. After losing jobs selling merchandise at concerts and cutting fabric for Hollywood sets, she is more than $10,000 behind on rent.

Debt threatens to hit renters in several ways. Some have kept up with their rent payments but have turned to credit cards and high-interest loans. Others owe mounting bills directly to landlords that must be paid back when eviction moratoriums expire, opening the possibility — if the debt goes unpaid — for evictions and court orders for back rent. That could erode credit scores and lead to wage garnishments and more.

“We are setting up millions of people for long-term harm and a cycle of economic and housing instability,” said Emily Benfer, chair of the American Bar Assn.’s COVID-19 Task Force Committee on eviction.

Renters across the nation are dipping into 401(k)s, taking on higher-interest debt, and scrambling for risky, essential-worker jobs to pay the rent. Research from Moody’s Analytics and the Urban Institute estimates 9.4 million U.S. renter households owed an average of $5,586 in back rent, utilities and related late fees as of January, for a total burden of $52.6 billion.

Other estimates show a smaller but still significant amount of rent debt. The full scope of the problem isn’t clear because the situation is fluid, and estimates so far are based on surveys and models, rather than hard data.

“[Bad] debt affects your credit score, and credit scores affect everything in your life,” said Yuval Yossefy, a manager at the Legal Aid Foundation of Los Angeles, a nonprofit law firm.

Federal, state and local officials are grappling with how best to help people stay afloat — including keeping them housed — amid job losses, slashed incomes and pervasive disease. A second year of the COVID-19 pandemic has brought little reprieve, with new variants of the coronavirus threatening to accelerate the virus’ spread and cause longer disruptions to the economy and everyday life.

States are planning to get federal aid funds, which have begun to flow, into the hands of landlords to reduce the debt load on tenants. California, where median rent is 50% higher than in the nation at large, has passed what state leaders characterize as the strongest statewide measures to address the crisis, providing a potential model for how states could distribute rent funds.

The California measures, approved by the Legislature last week, extend a statewide moratorium on evictions for people with pandemic hardships through June. Significantly, they bar landlords from using rent debt accrued between March 2020 and June of this year to deny future housing — a nod to fears that unpaid rent may affect people’s housing for years to come.

And to protect the most vulnerable, they establish a program that uses federal stimulus money to encourage landlords to forgive debt accrued by low-income tenants over the span of a year: April 2020 to March of this year.

Whether California landlords opt in, exactly how the program will be implemented, and if it will make a significant difference for those most in debt are still open questions. Nonprofit groups that work with low-income renters say the measures could be hard to enforce and, in terms of altogether forgiving some debt, rely precariously on optional landlord participation.

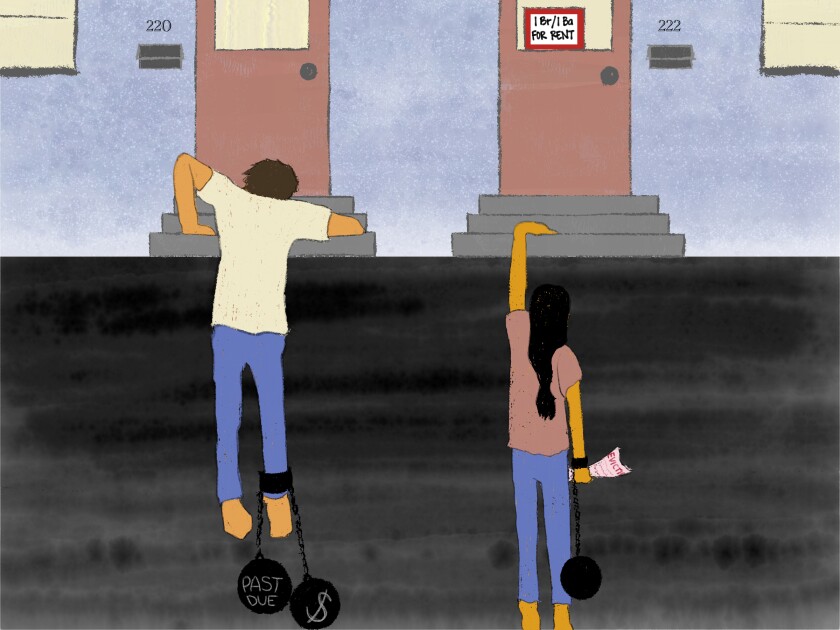

Eviction and debt can make it difficult to find new housing, take out loans, get some types of jobs or budget for necessities like food. In California, where rent was unaffordable for most tenants to begin with, the debt pile-on compounds a long-brewing problem.

Eviction and debt can make it difficult to find new housing, take out loans and get some types of jobs.

(Nicole Vas / Los Angeles Times)

“A family that makes less than $30,000 a year, they are going to be on the verge of homelessness for the next 10 to 15 years because of this huge debt,” said Ana Grande, associate executive director of the nonprofit Bresee Foundation in Los Angeles, which provides assistance to low-income families.

Making matters worse: Studies show those with debt are least likely to afford it — even if they regain their old incomes. Compared with all L.A. County renters, households that earned less than $25,000 in 2019 were more than twice as likely as all renters to not pay their rent during the pandemic, according to a joint USC-UCLA survey. Households that earned between $25,000 and $50,000 were the second most common group to report not paying.

Nonpayment was also highest among Latino and Black Americans who, compared with white Americans, have been hit harder by the health and economic effects of the virus. They are also less likely to have family who can lend financial help given the country’s long-running racial wealth gap.

An eviction ‘changes the trajectory of a life’

Across the country, a series of problems can unfurl from a single eviction.

Some landlords refuse to take tenants with an eviction on their record, while those who do are likely to charge more, fail to keep up their properties and have units located in dangerous neighborhoods, according to housing attorneys and other experts.

Studies have found people who are evicted are more likely to experience depression and to die of any cause. People move far from their support networks, or miss work while trying to find new housing and lose their jobs. Kids fall behind at school.

“An eviction is not a single event in a person’s life,” Benfer said. “It actually changes the trajectory of a life, because it has such catastrophic implications for fiscal and mental health.”

In a pandemic, experts say an eviction is particularly dangerous, leading a person to double up with friends and family in crowded housing situations that accelerate the virus’ spread.

Absent an eviction on a person’s record, debt and poor credit scores can impede the ability to find housing, often leaving people to live in lower-quality conditions, said Ariel Nelson, an attorney with the National Consumer Law Center.

Poor credit scores also limit the ability to take out car, home and other loans at reasonable interest rates, putting homeownership further out of reach.

Past-due debts on a credit report may lead some employers to turn down a candidate for jobs that involve handling money, such as a bank teller or a cashier at a restaurant, said Bruce McClary, spokesperson for the National Foundation for Credit Counseling.

If debts continue to go unpaid, creditors can garnish wages, though restrictions exist on how much disposable income creditors can take.

To preempt this, people might dip into savings or cut back on food. They may take out the only loans available to them: sky-high-interest products that critics say are nearly impossible to pay back.

Some tenants have already headed down the debt spiral. The USC-UCLA study found 8.5% of surveyed tenants paid some rent with a credit card in July, compared with 3% normally. Nearly 8% used a payday or other emergency loan.

An out-of-work graduate student in Lakewood told The Times she requested and got a budget increase for her student loan to pay rent, adding to her total student loan load. A laid-off worker in the concert industry said they used a 401(k) loan. Some people interviewed said they had already dipped into their savings.

Lamonte Goode, a 44-year-old dancer, says he may tap his savings to begin paying the roughly $10,000 in back rent he owes. With COVID-19 restrictions halting TV shows and theater performances, Goode said he hadn’t found steady work since March and was looking for a job outside his field to pay bills. Unemployment hasn’t been enough to cover expenses, including the $1,800-a-month rent on his one-bedroom in West Hollywood, he said.

Asked if he thought he would be able to repay the debt, Goode said he didn’t know and that he was trying hard to come up with the money. He also raised the question: Should the burden fall on him? “I am not the reason COVID is happening. Yet I still have to pay the debt for something I am not in control over.”

“The fact that someone lost their job and couldn’t keep up on rent is a very unique and extreme circumstance and does not and should not have a bearing on their creditworthiness for this next almost-decade,” said Nisha Kashyap, a staff attorney at the pro bono law firm Public Counsel, citing how long bad debts typically stay on a credit report.

“This is a global pandemic that came out of nowhere.”

Sid Lakireddy of the California Rental Housing Assn., which represents landlords in the state, says he believes fears of mass evictions and long-term harm to credit are overblown. Most landlords would rather work with their tenants on repayment plans than fight in court over an eviction or debt, he said, particularly since vacancies have risen in many cities. “The last thing we want is to put a good tenant out on the street.”

The federal government and state and local officials say they are trying to help both tenants and small landlords, who are also struggling.

Then-President Trump signed a bipartisan stimulus bill in December that approved $25 billion in rent and utility relief funds nationwide. President Biden extended the national eviction moratorium for people with pandemic hardships until the end of March, though critics say that ban is weak.

The new California law is stronger and contains provisions to reduce the likelihood that pandemic debt will have wide ripple effects.

Under the law, landlords cannot sell or assign any rent debt accrued during the pandemic until July 2021.

Russ Heimerich, a spokesman for the state’s Business, Consumer Services and Housing Agency, said the law goes even further for low-income tenants with pandemic hardships: It forever bars landlords from selling rent debt accrued through June.

That would prevent a primary way credit scores could take a hit, since it’s usually debt collectors rather than landlords who report to the credit bureaus, said Nelson, the attorney. Heimerich said the law also included several incentives for landlords to participate in the rent relief program for low-income tenants, and that making it mandatory would have been legally impractical.

Still, critics of the law say it relies too much on tenants knowing their rights and having the means to exercise them, putting the least-resourced in a weak position to benefit.

Some tenants have already been evicted, said Stephano Medina, an attorney with the Eviction Defense Network, during a recent news conference held online by tenant advocates on their concerns about the law. Moratoriums don’t stop landlords from filing cases, and tenants sometimes don’t realize they need to show up in court to defend themselves, Medina said.

One part of the law that is likely to be particularly hard to enforce is a clause that prohibits landlords from denying housing based on rent debt accrued during the pandemic, said Leah Simon-Weisberg, legal director with Alliance of Californians for Community Empowerment, an organizing group that advocates for low-income households. Prospective landlords often screen tenant candidates through their former landlords, allowing them to learn of debts they aren’t supposed to base decisions on.

It’s also unclear how many landlords will participate in the state’s rent relief program, which will pay landlords 80% of what they are owed if they forgive the remaining 20%. Lakireddy said that’s a good deal, and many landlords are likely to accept it.

California’s rent-control laws may complicate the landlord’s decision, said Tina Rosales, a lobbyist with the Western Center on Law and Poverty. Under state law, landlords can charge as much as they can get for a rent-controlled unit once it becomes vacant. So it could be more lucrative to pursue an eventual eviction and not forgive debts if a tenant is paying significantly below market rates.

“It has the potential for landlords to pick and choose which tenants they will participate in the program with,” Rosales said, potentially affecting the most vulnerable.

Another outstanding question is how far California’s rental relief funds will go, given the range of estimates of how much rent people owe. Some tenants, for example, might miss out on debt forgiveness — not because their landlord won’t participate but because the pool of money runs out.

For many who can’t work from home, the cost of staying housed becomes a choice between incurring debt or accepting the risk of contracting COVID-19 on the job.

One family’s hard choices

The Buenos, a family of five in Los Angeles’ Koreatown neighborhood, were like many of the country’s hardworking households. Fernando prepped fish for a sushi chain. His wife, Maribel, cooked at a downtown L.A. brunch spot.

Maria, 23, the eldest of three sisters, worked at a big-box retailer and helped out with the family bills. She set a goal to own her own home by 30.

The Buenos are now scattered. A promotion sent Maria’s father to New Jersey before the pandemic, but his hours were soon cut as lockdowns were put in place. Her mother lost her job and moved across the country with her youngest daughter to join Fernando.

At home in Koreatown, the bills fell on Maria, who stayed behind with her 18-year-old sister, Pamela. Their parents send money, but even coupled with Maria’s $20-an-hour wage, it’s not enough to cover the $2,500 in monthly rent. She exhausted her $3,000 in savings and is still $15,000 behind on rent.

Maria worries about how she’ll protect her younger sister and keep both of them from becoming homeless.

James Engel, a principal with the company that manages Bueno’s building, said the company planned to work with residents on multiyear repayment plans when rent protections expire, rather than pursue evictions and collections. He wouldn’t comment on individual tenants’ cases.

Maria says she doesn’t want to risk having the debt over her head and is looking for a second job during the pandemic.

The possibility of getting sick is a sacrifice she’s willing to make.